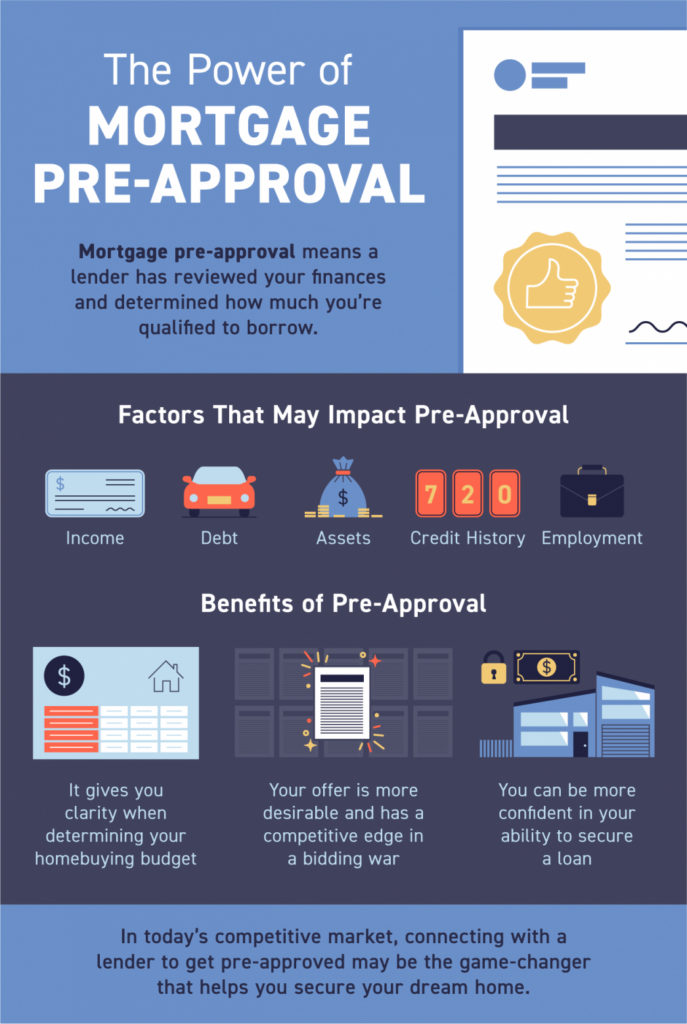

Mortgage Pre-Approval is the most critical first step in the homebuying process. It not only helps you understand your budget and financing options but also positions you as a serious buyer in the eyes of sellers. In today’s competitive real estate market, having a Mortgage Pre-Approval gives you a clear advantage, allowing you to act quickly and confidently when you find the perfect home.

By securing a Mortgage Pre-Approval, you’ll gain insight into your loan amount, potential interest rate, and monthly payment options. This knowledge empowers you to make informed decisions while streamlining the entire homebuying experience. In this blog, we’ll explore why Mortgage Pre-Approval is essential, how it works, and how it sets you up for success on your journey to homeownership.

What Is Mortgage Pre-Approval?

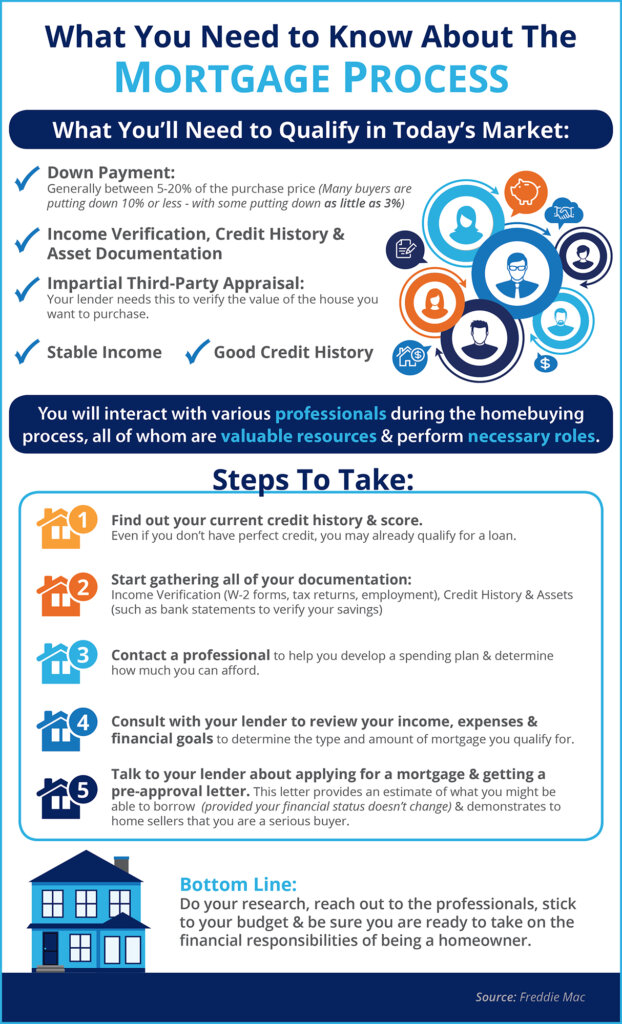

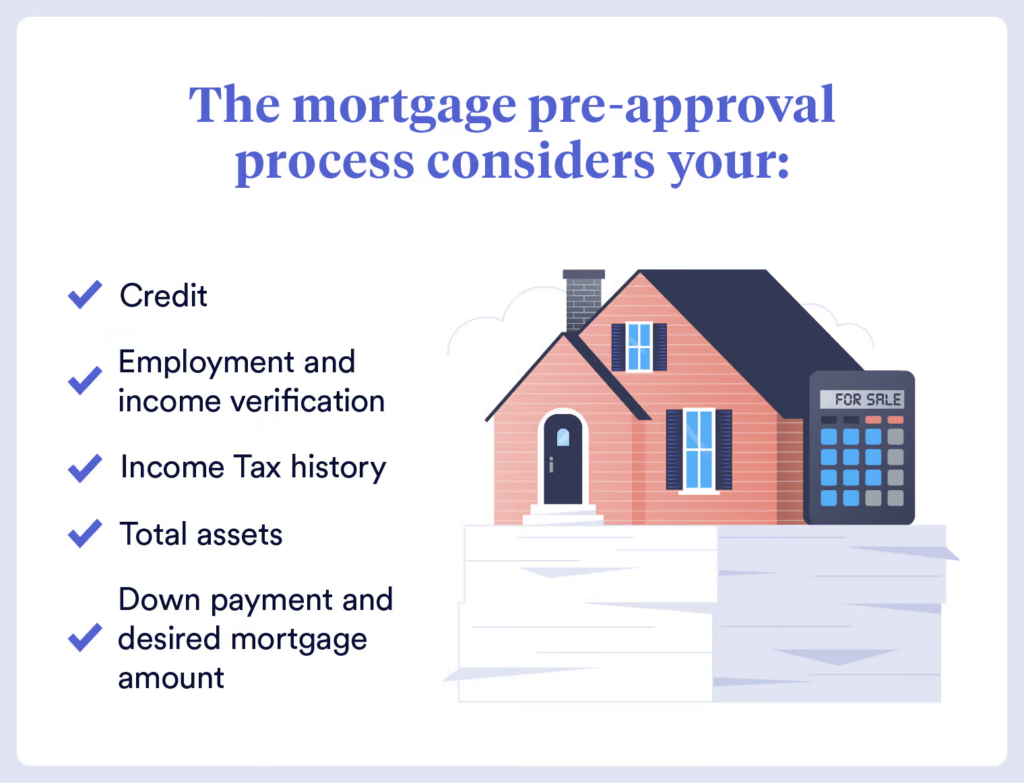

A mortgage pre-approval is a crucial step in the homebuying process. It involves a formal evaluation of your financial situation—such as income, credit score, debts, and assets—by a lender to determine how much they’re willing to lend. Unlike pre-qualification, which offers a rough estimate, pre-approval includes a thorough review of your financial documents and credit, making it a more accurate gauge of your borrowing power.

With pre-approval, you’ll have a clear idea of how much home you can afford and your potential monthly payments. This not only helps you focus your search on homes within your budget but also shows sellers you’re a serious buyer with financing already underway, which can make your offer stand out in a competitive market.

The Mortgage Pre-Approval Process

Embarking on the Mortgage Pre-Approval journey is a pivotal step in the homebuying process. This procedure involves a comprehensive evaluation of your financial health by a lender to determine the loan amount you qualify for. Here’s a breakdown of the key components involved:

Personal Identification

- Government-Issued ID: A valid driver’s license, passport, or state ID to confirm your identity.

Income Verification

- W-2 Forms: Documents from the past two years to verify your employment and income history.

- Recent Pay Stubs: Typically from the last 30 days, these provide current income details.

- Tax Returns: Complete returns from the past two years offer a comprehensive view of your financial standing.

Asset Documentation

- Bank Statements: Statements from the last 60 days for all checking and savings accounts to demonstrate available funds.

- Investment Account Statements: Recent statements from retirement accounts, stocks, or other investments, if applicable.

Debt Information

- Credit Report: A detailed report highlighting your credit history and current obligations.

- Debt Statements: Information on existing debts, such as student loans, car loans, or credit card balances.

Residential History

- Proof of Residency: Documentation of your addresses for the past two years, which may include lease agreements or utility bills.

Upon gathering and submitting these documents, the lender will assess your financial profile. If you meet their criteria, you’ll receive a pre-approval letter specifying the loan amount you’re eligible for. This letter not only guides your home search by establishing a clear budget but also signals to sellers that you’re a serious and qualified buyer.

It’s crucial to maintain financial stability during this period. Any significant changes, such as switching jobs, applying for new credit, or making large withdrawals, can impact your pre-approval status. Therefore, it’s advisable to avoid major financial moves until after your home purchase is finalized.

By understanding and navigating the Mortgage Pre-Approval process diligently, you position yourself for a smoother and more confident homebuying experience.

Benefits of Mortgage Pre-Approval

Obtaining a Mortgage Pre-Approval offers several significant advantages that can streamline your homebuying journey and strengthen your position in a competitive market:

1. Accurate Budgeting

A pre-approval provides a clear understanding of how much you can borrow, allowing you to focus your home search within a realistic price range. This prevents the disappointment of considering homes beyond your financial reach and saves time by narrowing your options to properties you can afford.

2. Enhanced Buyer Credibility

Sellers often prefer offers from pre-approved buyers, as it indicates that the buyer’s financing is likely to proceed without issues. This credibility can make your offer more attractive, especially in multiple-offer situations, giving you a competitive edge over other buyers who have not secured pre-approval.

3. Faster Closing Process

Since much of your financial information has already been reviewed during the pre-approval process, the time required to finalize your mortgage is typically reduced. This can lead to a quicker closing, allowing you to move into your new home sooner.

4. Better Negotiation Power

With a pre-approval in hand, you may have more flexibility in negotiating terms and pricing. Sellers are more likely to engage with buyers who have demonstrated their financial readiness, potentially leading to more favorable terms for you.

5. Identification of Potential Financial Issues

The pre-approval process involves a thorough examination of your financial situation, which can help identify and address potential issues early on. This proactive approach allows you to resolve any problems before they can derail your home purchase plans.

By securing a Mortgage Pre-Approval, you not only clarify your financial standing but also position yourself as a serious and prepared buyer, enhancing your chances of a successful and efficient home purchase.

Common Misconceptions About Mortgage Pre-Approval

While Mortgage Pre-Approval is an essential step in the homebuying process, several misconceptions often create confusion for buyers. One of the biggest myths is that pre-approval guarantees you a loan. In reality, pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a certain amount. However, final approval depends on additional factors, such as the home’s appraisal, updated financial documents, and maintaining your credit and income levels throughout the process.

Another misconception is that pre-approval lasts forever. Most pre-approvals are only valid for 60 to 90 days, after which they expire. If your homebuying timeline extends beyond that, you’ll need to renew your pre-approval by providing updated financial information. Additionally, many buyers mistakenly believe that pre-qualification is the same as pre-approval. While pre-qualification provides an estimate based on self-reported details, pre-approval involves a detailed review of your financial documents and is a much stronger indicator of your buying power.

There’s also a common concern that pre-approval will hurt your credit score. While the process does include a hard credit inquiry, the impact on your credit score is typically minor and temporary. The benefits of knowing your borrowing capacity far outweigh the slight dip in your score. Some buyers also fear that pre-approval limits their home search or locks them into a specific lender. However, pre-approval simply establishes a budgetary framework, and you’re still free to shop for the best interest rates and loan terms.

Finally, many buyers mistakenly believe that once they’re pre-approved, their financial behavior no longer matters. Any major financial changes—such as opening new credit lines, changing jobs, or making large purchases—can jeopardize your pre-approval status. It’s crucial to maintain financial stability until after closing to ensure a smooth transaction.

Understanding these misconceptions about Mortgage Pre-Approval can save you from potential surprises and help you make confident, informed decisions throughout your homebuying journey.

Maintaining Your Mortgage Pre-Approval Status

After securing your Mortgage Pre-Approval, maintaining it is just as important as obtaining it. Many buyers don’t realize that changes to their financial situation can jeopardize their pre-approval status, potentially delaying or derailing their home purchase. To avoid these pitfalls, it’s crucial to stay financially stable throughout the homebuying process.

- Avoid Major Financial Changes

Your lender bases your pre-approval on the financial information you provided at the time of application. Any significant changes, such as switching jobs, reducing your income, or taking on new debt, can alter your qualifications. For example, applying for new credit cards, financing a large purchase like a car, or co-signing a loan could affect your debt-to-income ratio and your ability to qualify for the mortgage amount.

- Don’t Make Large Withdrawals or Deposits

Large, unexplained bank transactions can raise red flags for lenders. If you need to move funds between accounts or receive a large deposit, ensure you have proper documentation to explain the source. For example, a gift from a family member may require a gift letter, and transferring funds for your down payment should align with lender requirements.

- Keep Your Credit Score Intact

Lenders will often re-check your credit score before closing. Missing a payment, maxing out credit cards, or making late payments can negatively impact your score and potentially disqualify you from your pre-approved amount. To maintain your credit score, continue making payments on time and avoid taking on additional credit.

- Stay in Touch with Your Lender

Maintaining open communication with your lender is vital. If you anticipate any changes to your financial situation, notify your lender immediately. They can guide you on how to handle these changes without jeopardizing your pre-approval. Regular check-ins can also ensure your pre-approval remains valid if your home search takes longer than expected.

- Be Aware of Pre-Approval Expiration

Most pre-approvals are valid for 60 to 90 days. If your homebuying process extends beyond that, you’ll need to renew your pre-approval by providing updated financial information. Keep track of your pre-approval’s expiration date and plan to update your documents to avoid any interruptions.

By following these guidelines, you can safeguard your Mortgage Pre-Approval and ensure a smooth path to purchasing your dream home. Remember, financial stability is key to successfully navigating the homebuying process and closing on your new property without unnecessary delays.

The Role of Mortgage Pre-Approval in Competitive Markets

In today’s competitive real estate market, obtaining a Mortgage Pre-Approval is a strategic move that can significantly enhance your homebuying experience. A pre-approval not only provides a clear understanding of your budget but also positions you as a serious buyer, giving you a competitive edge.

One of the primary advantages of pre-approval is the ability to act swiftly when you find your ideal home. Since your financial information has already been reviewed, the mortgage process is expedited once your offer is accepted, allowing you to close faster. In a hot market, speed is crucial.

Moreover, pre-approval provides clarity on exactly how much you can afford. This prevents time wasted on properties outside your budget and helps you focus on the right homes.

Additionally, pre-approval strengthens your ability to negotiate house prices when buying a home. Establishing credibility through pre-approval is essential in competitive markets, as it demonstrates to sellers that you have the financial backing to proceed with the purchase.

By securing a mortgage pre-approval, you not only streamline your home search but also enhance your standing in a competitive market, increasing the likelihood of a successful purchase.

The Power of Mortgage Pre-Approval: Final Thoughts

In the homebuying journey, few steps are as critical as securing a Mortgage Pre-Approval. From providing clarity on your budget to positioning you as a credible and competitive buyer, pre-approval is the foundation that sets you up for success. In today’s fast-paced real estate market, where homes can receive multiple offers within hours, having a pre-approval letter not only gives you confidence but also demonstrates to sellers that you’re ready to close the deal.

By understanding the process, avoiding common misconceptions, and maintaining financial stability, you can make the most of your pre-approval status. Remember, pre-approval is not just about getting a green light from your lender—it’s about preparing yourself for a seamless, informed, and empowered homebuying experience. Whether you’re navigating a competitive market, negotiating with sellers, or working to avoid surprises along the way, Mortgage Pre-Approval is your key to opening the door to your dream home.

If you’re ready to start your homebuying journey or have questions about getting pre-approved, reach out today for personalized guidance. Let’s work together to make your dream of homeownership a reality!