What does rising housing inventory in Washington state mean for buyers and sellers in 2026? Washington’s active home listings have surged to 21,381 by May 2026, giving buyers more choices and negotiating room while pushing sellers to price and market homes more strategically than they have in years. New tax legislation, mortgage rate pressures, and shifting migration patterns are all contributing to this change.

Washington’s housing market is sending a clear signal in 2026: more homes, slower sales, and sellers who can no longer rely on automatic offers.

That’s a meaningful shift from the past few years, when listings evaporated within days and buyers routinely outbid each other just to get a house. The energy in the market feels different now. Not panicked, not crashed, but deliberately slower. Buyers have options. Sellers have competition. And everyone is recalculating.

If you’ve been watching from the sidelines as a buyer waiting for inventory, or as a seller trying to read the room, this is the update you need. We’ll look at what the data actually shows, what’s driving the change, how Washington’s rapidly evolving tax landscape fits into the picture, and what smart buyers and sellers are doing right now.

What the Numbers Actually Say

If you’ve been house hunting in the Seattle area lately, you’ve probably noticed something that wasn’t true a year ago: there are simply more homes to choose from.

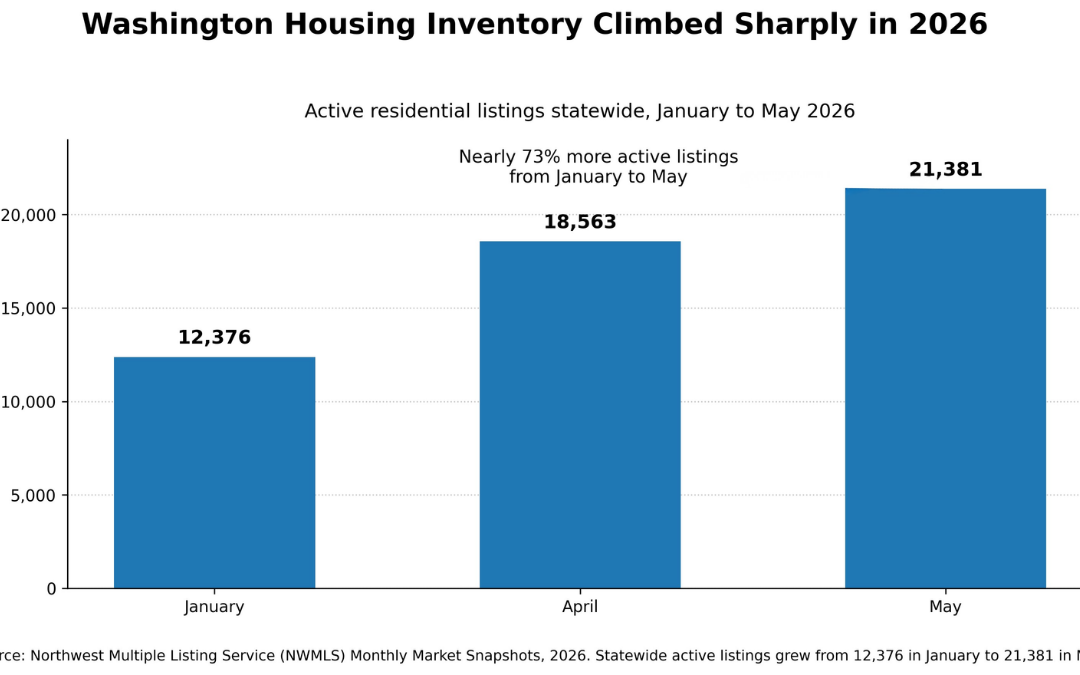

According to the latest data from the Northwest Multiple Listing Service (NWMLS), housing inventory across Washington State has been climbing steadily throughout 2026, while sales activity has remained relatively soft. The result is a market that feels very different from the intense seller’s market conditions many buyers and sellers became accustomed to during the pandemic years.

Statewide active listings increased from 12,376 homes in January 2026 to 21,381 homes in May 2026, representing nearly 73% inventory growth in just five months. At the same time, closed sales have struggled to keep pace. January sales were down 7.0% year-over-year, April sales were down 3.7%, and May sales were down 3.9% compared to the same months in 2025.

Meanwhile, home prices have largely stabilized. The statewide median sales price was $650,000 in both April and May 2026, essentially unchanged from a year earlier. That’s a major shift from the double-digit appreciation rates buyers experienced between 2020 and 2022.

For buyers, this means more options, more negotiating power, and less pressure to make rushed decisions. For sellers, it means pricing strategy, presentation, and marketing are becoming increasingly important as competition increases.

This Is Not 2008 — But It Is a Real Shift

Before anyone spirals, let’s put these numbers in context. This is a rebalancing, not a collapse.

Months of inventory statewide reached 3.44 in May 2026, up from about 2.4 a year ago. King County shows 3.4 months, up from 2.8 in May 2025. Both figures still sit below the 4-6 months typically associated with a balanced market. We are not in buyer’s market territory yet. But we’re getting closer than we’ve been in years.

And buyer activity is real. In May, keybox accesses at listed properties increased 12.2% month-over-month. Showings rose 5% from April. Pending sales increased 7.7% from April and closed sales rose 9.5% month-over-month as the spring market picked up. Buyers are out there. They’re just moving more deliberately and with more leverage than they had a year ago.

The difference between this market and 2021-2022 is not that buyers have disappeared. It’s that buyers have choices now, which means sellers have to earn the sale rather than simply show up.

How Different Counties Are Trending

The inventory surge is not uniform across Washington. Some counties are seeing dramatic increases:

King County’s 25.6% increase is notable because it’s the state’s most expensive and most competitive market. The fact that inventory is rising significantly even there signals a broader structural shift, not just a rural softening.

Why Are More Homeowners Listing Now?

Several forces are converging at the same time, and they’re affecting different homeowner types in different ways.

The rate lock effect is loosening. The single biggest factor suppressing inventory over the past two years has been homeowners who refinanced at 2-3% rates in 2020 and 2021 and had zero incentive to give those loans up. Listing a home means buying your next one at 6.5-7%, which can mean hundreds of dollars more per month on a comparable property. But life circumstances don’t wait: retirements, relocations, divorces, estate sales, health changes, and job moves are forcing the issue regardless of mortgage rates. The pent-up supply that was locked behind rate psychology is slowly releasing.

Equity-rich sellers still have room to move. Seattle-area homeowners who bought before 2020 are sitting on substantial equity. A home purchased for $550,000 in 2018 may be worth $850,000 or more today. That equity cushion gives sellers flexibility. Even buying at a higher rate, many can right-size into a smaller home, relocate to a lower cost-of-living area, or pull equity out for retirement. The math still works for a significant portion of long-term owners.

Life transitions are accelerating. The Baby Boomer generation is at peak estate and retirement transition age. In the Greater Seattle area, which has an aging homeowner base in many established neighborhoods, the natural churn of estate sales, downsizes, and senior relocations is adding meaningful supply to the market. This trend will continue for the next decade regardless of interest rates or prices.

Washington’s shifting tax environment is a factor. For high-net-worth homeowners and retirees especially, the state’s evolving tax picture is entering the conversation around where to live in the next chapter. We’ll cover that in detail below.

The Tax Picture: What Washington Homeowners Need to Know in 2026

Washington has long attracted residents and businesses with its lack of a traditional state income tax. That advantage has narrowed considerably in 2026, and for certain homeowner profiles, the implications are significant enough to drive relocation decisions.

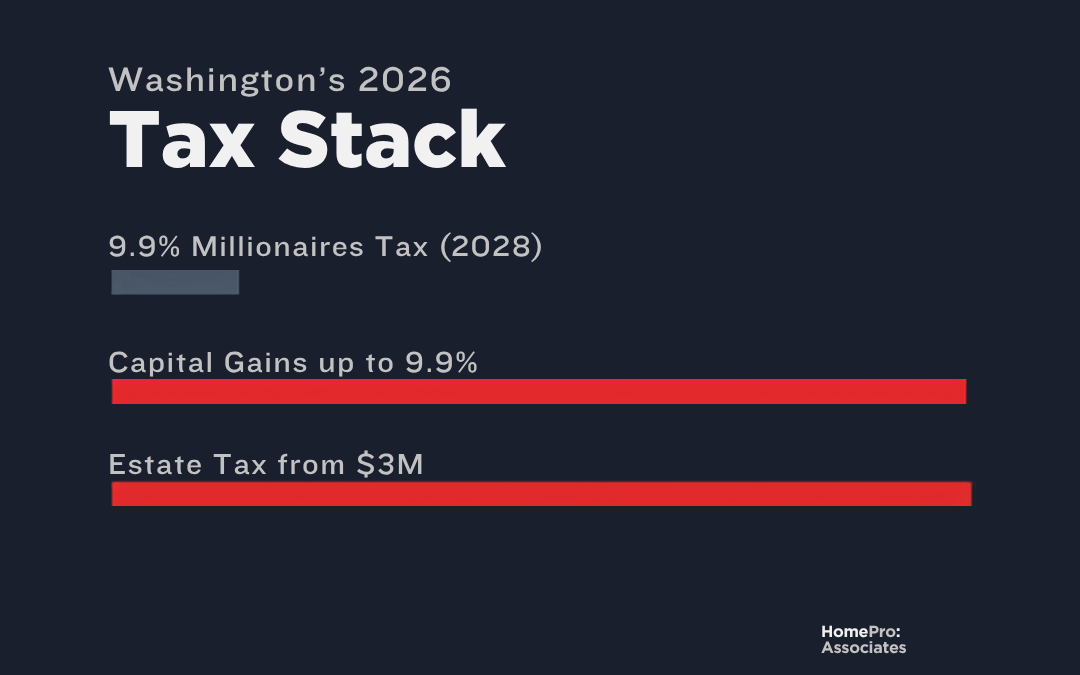

The Millionaires’ Tax (SB 6346)

Governor Bob Ferguson signed Senate Bill 6346 into law on March 30, 2026. The law imposes a 9.9% rate on household income above $1 million per year, effective January 1, 2028, with first returns and payments due in April 2029.

Washington lawmakers approved a new tax on household income above $1 million, which supporters and critics continue to debate and which remains subject to legal and political challenges. The law is estimated to generate $2-3 billion annually for the state. It is currently facing legal challenges, and a voter initiative effort is working to put a repeal measure on the November 2026 ballot. So the landscape may shift again. But for planning purposes, high-income households are treating it as real until a court or voters say otherwise.

Does this affect home sales directly? No. Residential real estate gains remain exempt from Washington’s capital gains excise tax, so the act of selling your home is not directly affected by SB 6346. However, for tech executives with large annual equity income, business owners expecting a liquidity event, and investors with substantial non-real-estate income, the calculus around Washington residency is changing. That shift is beginning to show up in conversations about where to live, which affects demand at the higher end of the market.

Capital Gains Tax: The Current Structure

Washington’s capital gains excise tax has been in place since 2022 and was upheld by the Washington State Supreme Court in 2023. As of 2025, it operates on a tiered structure:

| Gain Amount | Rate | Notes |

|---|---|---|

| Up to ~$278,000 | 0% (exempt) | Standard deduction, adjusted annually for inflation |

| $278,000 to $1 million | 7% | Applies to the gain above the standard deduction |

| Above $1 million | 9.9% | Rate increase effective retroactively January 1, 2025 |

| Real estate gains | Exempt | Both residential and commercial property are exempt |

| Retirement account distributions | Exempt | IRA, 401(k), 403(b), pension distributions all excluded |

Source: Helsell Fetterman 2026 Estate Planning Update. Most homeowners selling a primary or investment property are not directly affected by this tax.

This tax primarily affects tech workers exercising large stock option grants, founders and business owners selling a company, and investors liquidating significant non-real-estate portfolios. If that describes you or someone in your household, talk to a CPA before making any major financial decisions.

Estate Tax: The Gap Between Washington and Federal Law

Washington has one of the most aggressive state estate taxes in the country. Following legislative adjustments under SB 6347, effective July 1, 2026 the structure is:

| Threshold | Washington State | Federal |

|---|---|---|

| Exemption (2026) | $3,076,000 per person | $15,000,000 per person |

| Top rate (post July 1, 2026) | 20% | 40% |

| Couples (combined exemption) | ~$6,152,000 | ~$30,000,000 |

Source: Washington Estate Tax 2026 (Jensen Estate Law) | Helsell Fetterman 2026 Update

That gap between the state and federal exemptions is what catches families off guard. A paid-off Seattle-area home worth $900,000 combined with a retirement account, an investment portfolio, and a small business interest can cross Washington’s $3 million threshold faster than most people expect. Married couples may be able to utilize both spouses’ exemptions through proper estate planning. Families in that range may owe significant Washington estate tax even though they are far below the federal threshold and may not think of themselves as wealthy enough to worry about it.

For retirees and long-term homeowners thinking about their next chapter, estate planning considerations are increasingly shaping where they choose to live.

Are People Actually Leaving Washington?

This is the question I get asked more than any other right now, and the answer is: some are, most aren’t, and the data is more nuanced than the headlines suggest.

Online commentary and anecdotal reports from agents across the state do point to an uptick in retirees and high-earners evaluating moves to states like Nevada, Arizona, Idaho, Texas, and Florida. These states share a few characteristics:

- No state income tax

- No estate tax

- Lower overall cost of living

- Warmer climates for retirees

- Uncertainty about WA tax trajectory

- World-class job market (tech, aerospace, healthcare)

- Long-term real estate appreciation history

- Natural beauty and lifestyle advantages

- Family, community, and social ties

- No sales tax in some border areas

Washington has powerful economic anchors, Amazon, Microsoft, Boeing, and a thriving healthcare sector, that are not going anywhere. The people most likely to leave are those for whom income and estate taxes represent a genuinely meaningful annual cost, typically households earning well above $500,000 per year or those sitting on estates approaching or exceeding $5 million. That’s a real segment of the Greater Seattle market, but it’s not most homeowners.

Migration trends take years to show up in home price data. What we’re likely seeing in the inventory surge is less about people leaving and more about the general cooling of pandemic-era urgency, rate dynamics, and life transitions that were always going to produce a wave of listings in this period.

Bottom Line on Migration

Washington remains a strong long-term real estate market. The fundamentals: job growth, population base, geographic constraints on supply, and quality of life, support home values over time. The tax changes are real and worth factoring into your financial planning, but they are not a reason to panic about the market collapsing. This is a market that is adjusting, not unraveling.

What This Means If You’re a Buyer in 2026

If you’ve been waiting for the market to give you a breath, this is it. Not a crash landing, but a real window of opportunity that did not exist 18 months ago.

What Has Improved for Buyers

- More homes to choose from across King and Snohomish Counties than at any point in the past four years

- Less bidding war pressure, particularly on homes priced above $800,000

- More room to ask for inspections, repair credits, and contingencies without automatically losing

- King County inventory up from 2.2 to 3.4 months of supply over the past year

- Sellers more willing to negotiate on price and terms

What Still Challenges Buyers

- Median price still $650,000 statewide, with King County homes considerably higher

- Mortgage rates remain elevated at 6.5-7%+, limiting purchasing power

- Down payment requirements in this price range remain substantial

- Well-priced homes in desirable neighborhoods still move quickly

- Competition from all-cash buyers in certain price segments

The best strategy for buyers right now is to get pre-approved, know your number, and be ready to move when the right home comes up. The days of needing to waive every contingency just to compete are fading, but this is not a sleepy market where you can drag your feet. Prepared buyers are still winning. Unprepared buyers are still losing to someone who did their homework.

If you are relocating to the Seattle area from out of state, the Eastside communities of Bellevue, Kirkland, Redmond, and Bothell remain the highest-demand submarkets. Seattle proper and the north end, Shoreline, Kenmore, Bothell, offer meaningful value at lower price points than Bellevue. Snohomish County, including Edmonds, Lynnwood, and Bothell, continues to attract buyers priced out of King County.

What This Means If You’re a Seller in 2026

The autopilot listing strategy is over. Pricing 10% above market and waiting for escalation clauses to roll in is a strategy that stalls in this environment.

With 21,381 homes on the market across Washington, buyers have options they did not have two years ago. They will walk past an overpriced home without a second thought when there are four comparable homes a short drive away. That’s a fundamentally different dynamic than what sellers experienced in 2021-2022.

Here’s what the sellers who are actually closing deals in 2026 are doing differently:

The benchmark is what comparable homes sold for in the last 60-90 days, not what your neighbor got in April 2022. A Comparative Market Analysis from a local agent using current InfoSparks MLS data gives you a defensible number. Overpricing costs you time, and in this market, time on market creates buyer skepticism that compounds.

Staging, professional photography, and curb appeal work matter more when buyers have real alternatives. A home that photographs poorly or shows as cluttered and dated will lose to a similar home that shows beautifully, every time. Deep cleaning, fresh neutral paint, and landscaping cleanup are the highest-ROI moves before any listing.

Spring and early summer are historically the strongest windows in the Pacific Northwest, and we are in that window right now. Listing in June means competing against peak inventory but also targeting peak buyer demand. Fall listings tend to face less competition but also fewer motivated buyers. If you are on the fence, sooner is generally better in 2026.

In a high-inventory market, passive exposure is not enough. Maximum MLS syndication, social media promotion, targeted digital advertising, and YouTube video exposure all matter. Buyers are doing more online research before scheduling showings than ever before. A home that shows up everywhere gets shown. A home that relies only on MLS gets overlooked.

If you’ve had 10 or more showings with no offers in the first two weeks, the market is telling you something about the price or the condition. Acting on that signal early, with a price adjustment or targeted improvements, puts you ahead of sellers who wait six weeks and then panic. The best agents have a system for tracking showing feedback and guiding sellers on when and how to respond.

Sellers who treat their home like a product, priced accurately, presented well, and marketed aggressively, are the ones reaching the closing table in 2026.

The Bottom Line: This Market Rewards Strategy

Washington’s housing market in 2026 is not a crash, a bubble, or a reason to panic in any direction. It’s a market that has returned to something closer to normal after several years of historically abnormal conditions. More inventory, more careful buyers, flat-to-softening prices, and sellers who need to work harder to close deals.

For buyers, that means real opportunity to get into a home with reasonable terms, contingencies, and time to make a thoughtful decision.

For sellers, it means strategy matters in a way it simply didn’t in 2021. The homes that sell quickly are the ones that are priced right, look great, and are marketed well. The homes that sit are the ones that aren’t.

And for anyone with a more complex financial picture: high equity, significant investment assets, a business, or estate planning concerns, the tax changes in Washington deserve a conversation with both a real estate professional and a financial advisor before making any major moves.

If you want a clear-eyed look at what this market means for your specific situation, that’s exactly what I do. No guesswork, no pressure. Just honest advice grounded in current data.

Frequently Asked Questions

Let’s Build Your Strategy for This Market

Whether you’re thinking about selling, buying, or just want to know what your home is worth right now, I’ll give you straight answers based on current data, not guesswork. No pressure, no obligation.

Text HOME to 206-245-8813 and I’ll send you our free seller strategy guide.

Warmly, Emily