Does House Hacking in Seattle, WA even WORK?

Okay guys. So today, I want to talk a little bit more about house hacking in the Seattle market. I actually get a lot of interest on my website from people who are looking for investments and a smart way to enter the Seattle market.

I’ve done some other videos about investing in Seattle (specifically in Shoreline here where I live) and just the difficulty of doing it because of the negative cashflow situation. It’s one thing if you’re a high income earner, maybe you’re a doctor, you’re an IT guy, that you’ve got a lot of money coming in and you need that tax write off. And so it’s okay to lose a little bit of money every month because you’re making it up in appreciation. I’ve got another video on that, but that is not for everybody. And it’s certainly a difficult place to start. Today we’re going to talk about something else fairly different – House Hacking in Seattle, WA!

Have You Read About House Hacking on Bigger Pockets?

If you’re just out of school, you’re just in your first job, you may have gone to Bigger Pockets, which is a fabulous website. BiggerPockets.com is a discussion board, a forum. It’s free. It’s a great place for people to connect and discuss rehabbing, landlording, Air BnB, that type of a thing. And so it’s a good resource for you. And I got started with books and audio cassettes (what!?!?) and many thousands of dollars of investing materials and education to get me started on my investing journey, but now with the internet, a lot of free information is available to you – you just have to be willing to sift through it. (In real estate as in other investments, you usually have to invest Time or Money… or work with someone who has already invested those things and knows the ropes).

So, if you’ve read Scott Trench’s book (the CEO of Bigger Pockets), heard his podcast, or just hung out on the message boards these days, you may have heard the term “house hacking” and may be wondering if this will actually still work for you, given all the changes in the market lately, and the fact that Seattle is a very expensive place to live!

So let’s dive in to some of the numbers. This is based on things that I’ve been talking about with some of my clients lately, so it’s fresh on my mind.

What Is the Seattle Real Estate Market Really Like?

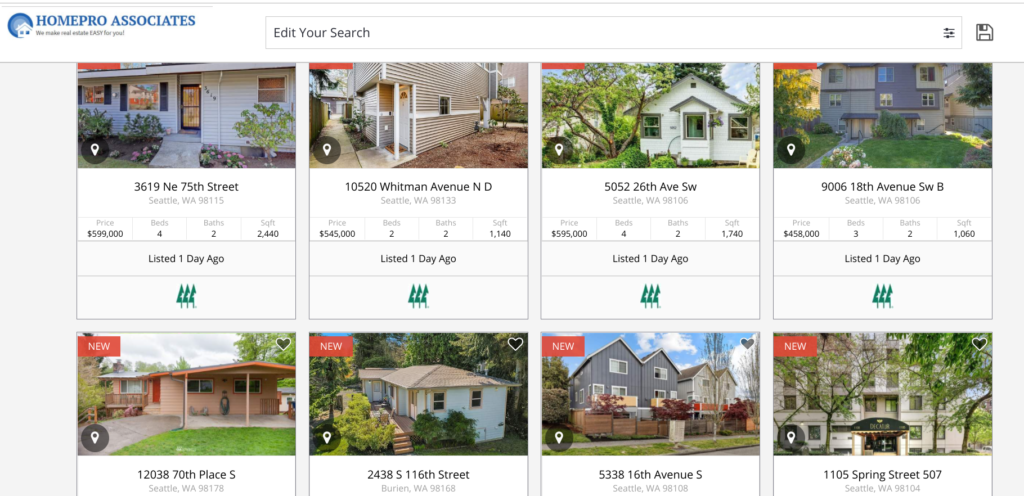

So let’s go to my property website and take a look at what’s available in Seattle. I’m just going to try looking for things that are under $600,000 and with at least two bedrooms. And the reason that I’m choosing these parameters is because if it’s much above $600,000, getting something to cashflow is very difficult. And the type of house hack that we’re going to be talking about here is the type where you have roommates.

Roommates Are The Secret To Your Success (Choose Wisely)

You might’ve heard David Green on the Bigger Pockets podcast talk about using this method in California. He’s a retired police officer who was working crazy hours at his job as an officer, getting all sorts of overtime and money. And he had this big house and, as a single guy, he wasn’t really utilizing it. So what he did was he rented out other rooms to fellow officers at his workplace, and he was able to generate additional income from the vacant space in his house. If you’ve been coming out of college and you’ve had roommates in the college dorms or in an apartment at school, you’re probably used to living with other folks. Maybe you even have some friends that you’d like to continue to share space with.

So if you can work this out, it can be very pleasant and fun and nice, but there are a couple of things that we want to watch out for. So I’m going to go into that later. I’m just talking now about what kind of space we’re able to get for this price range.

So we can get houses or we can get condos. Some people prefer a house for more space and privacy. Some people prefer a condo for more community and less maintenance. Look at this. Here’s a house for $595,000. I’m seeing homes like this kind of in southwest Seattle, WA. And it has 4-bedrooms.

You can get a lot of good deals on this type of property in the south end. Check out what it’s like living in Renton, WA and see if that’s something you’d like to consider.

So this would be a fantastic one if you were open to having a house and a little bit of home maintenance. Some people like the hands-on aspect of home ownership and can find ways to improve the value. And some want it to be completely hands-off.

Which Type Of Investor Are You?

Some like the idea of kind of rolling up their sleeves, getting their hands dirty, going ahead and putting in that drywall or fixing things, redoing the carpet and flooring and that type of a thing. That’s a little bit easier to do in the empty side of a duplex or in a property that you haven’t moved into. It’s also one where maybe that the house is functional, but ugly. And you can do that remodeling on the way out before you sell the property or before you leave and lease it to a different tenant. But the rehabbing and modeling takes a little bit extra cash and or elbow grease. And it can be hard if you’re trying to keep the home fully occupied with tenants. So knowing ahead of time kind of what your strategy is and what your orientation is toward repairs can help you find the best fit.

Here’s another little 3-bedroom townhouse for $468,000. And this is not fancy guys, but for your first home, this is not bad. And it’s got nice inside, right? Maybe a little bit dated, but you could live with that. Look at those nice floors. And this one I’m guessing is also in South Seattle. Yeah. Delridge. Okay. There’s white center right there.

What About Buying A Seattle Condo To House Hack With?

So let’s look at this compared to something like a condo. So here’s a condo. This is a $600,000 condo. And it’s pretty nice as well. This is a three bedroom.

And so, what are your payments going to be on something like this? Well, let’s say $600,000 is your max. You can go here into the calculator and you can decide what your down payment is going to be. Now I will put you in touch with a lender if you’d like a recommendation or you can obviously choose your own lender, but most folks are not going in with a full 20% down in the Seattle market. It’s a lot of cash. The higher your down payment, the lower your payments will be each month. So if you do have cash or you’re getting a gift or an inheritance, or your parents are helping or anything like that, then that can be a good way to go to reduce your monthly responsibility. But let’s just say, you’re going in with 5% down. And this is the remaining mortgage balance.

You will also need some cash for your closing costs. So don’t use all of your cash for your down payment. You’re going to want some to pay all of the closing costs, basically for your loan and all of that. And then, the bank doesn’t want you to have $0 in the bank when you close on this property. So you’ll need to keep some cash reserves as well. Now, right now, interest rates are super low. I’m going to put in 4% as a placeholder there. I think there’ll be going up over time. And now, someone today was asking me how long of a loan term they should get. Dave Ramsey says 15 years is a great loan term, but in our high priced market, that can make your monthly payment very high. And that creates some extra risk if you lost your job or lost a tenant or something like that. You’d be out quite a bit of money each month.

Now, if you go to 30 years, which is what most people do, you’re going to have a much lower payment. And if something were to go sideways, it would be a little bit easier to cover that payment while you searched for a new tenant or got a new job or something like that. So this mortgage calculator is giving us our principal and interest. That’s what we owe to the bank, but you also have some additional fees that you need to pay. So one is property insurance. And in many cases with a condominium, that’ll be covered in the homeowners association. The homeowners association might also cover some of your utilities like water and sewer, that type of a thing. And then, you’ll also need to take a look at your property taxes. Now, I’ve pulled up a different property because the last one was new construction.

And it didn’t include all the information that I wanted to show you. But here, if you scroll down, you’ll see what the property taxes are. This in case, a little over $3,000. This is an annual fee. And it’s typically split up into two monthly payments by the county. So if it were $3,000 per year, you’d pay $1,500 in April and $1,500 in October. If you have a bank, typically they will roll that into your monthly payment so that you don’t have to worry about budgeting for it. The bank budgets it for you, and you just pay them the same amount each month. So it’s a little bit easier for you to plan.

The HOA is the homeowners association. This is the rules, the operators of the condominium development and these fees cover different things in different buildings. So for example, if you’re in a building with a lot of shared community space, a pool or rec room, hot tub, a rooftop garden, a TV room, all those sorts of amenities are going to be paid for by your homeowners association dues.

They also get to budget for all of the maintenance for the property. So when the building needs a new roof, or it needs to have a new parking lot paving done, or it needs new siding or new paint, new windows, those types of things are going to be covered by the homeowners association. And you would have to pay for them anyway, if you lived in a freestanding house. You just might not budget for each month. You might have to pay it all in one chunk down the road. So it’s just something to be aware of, that that’s part of what you pay for in a condominium. And it’s just structured a little bit differently than a home. So let’s say you got this place. This is a two bedroom condominium unit in Seattle, and the price is $340,000. So if you go in here and you put in your loan terms, you can actually get a pretty reasonable monthly payment.

So we’re going to start at $1,500 a month. Then we’re going to add in $400 a month for this HOA. And then this is going to be, let’s just call it, $300 a month to make it easy. So that’s $1,900. So that brings us to $2,200 per month for your monthly payments. So if you were in there with a roommate, you might each be able to pay about $1,100 per month for your share of the space. And you could be in there earning equity and building up equity over time and reducing your cost to live. If you live there by yourself, it would cost more. And even if you rented a place, you might rent something for just about that much or possibly more. Plus as a homeowner, there are some tax benefits. And then when you leave, it’s something that you can sell and you benefit from that.

Or you can keep, and you could continue to rent it out to somebody else who was going to rent either one of the rooms or the whole property. So if you did have a property manager, you would pay 10% of the income. So let’s say this unit was able to rent out for $2,500 per month. You would pay $250 per month to your property manager. And you could be out of states, living in a different location in a different country, and everything would be getting taken care of. That’s what I do with a lot of my out-of-state rentals. And it works very well. It’s a little bit easier than having to run over there when you need to show a property. If that’s not your main job, it can be kind of inconvenient.

So I just wanted to give you a sense of some of these numbers and how this could work. The most important thing is if you do get into a property like this, that you have your exit strategy in mind. I know a lot of today’s folks are kind of mobile and living in one place for the next 30 years doesn’t appeal to you. So if you did get into a property like this, I always recommend if you’re not planning to hold it for at least five years, it probably doesn’t make sense. There are enough transaction costs with the sale of the property that you’re just not going to make a lot of money if you have to resell again quickly to relocate. So either plan to hold onto it for a while, or don’t get in. If you plan to hold on to it for a while, you don’t have to live there the entire time. You can go ahead and keep it as a long-term rental.

Maybe when you get a better job or you get married or something changes with your income situation, you can keep this as an investment property while you’ve moved on to something else. Now, one more thing to keep in mind is that some of these condominiums do have rental caps. That means they don’t want too many of the units to be rented out. Sometimes banks or the other folks living there are afraid that a condominium development full of tenants will lower the property value. So in that case, you need to find out what the rental cap is. This will be available from the homeowners association and also how many of the units are currently rented. So for example, if one third of the units may be rented, are they currently renting one-third or do they just have a couple units? That’ll give you a sense of whether it’s likely that you’d be allowed that exit strategy.

Likewise, some condos now have become aware of Airbnb and have explicit rules that make it illegal to do short-term rentals of less than a month, for example. So even if you had a great location for your condo, if you wanted people coming in and out of there all the time, because it was a vacation rental or something like that, that may not be allowed by the homeowners association. So it’s another important due diligence item to take a look at.

How Can We Help You?

I would love to hear your questions. I know just getting your foot in the door of the Seattle real estate market can be difficult, but a couple more years of pain and sacrifice, living low on the land. Just kind of having a roommate, getting into position, writing that rising tide of appreciation. No promises that will continue, but Seattle has been very kind to us for… I’ve lived here for over 40 years. Well, I’m over 40 years old. I did go away for college though. But during that time period, the market’s been doing very well.

And even when it did dip after 2008, it has come back stronger than ever. So again, let me know what your questions are. This is kind of an exciting topic, but also it can be complicated and there are some nuances. I know I’ve been going pretty quickly through this, and I just want to make sure that I’m getting you guys the information that you need. So ask your questions, be sure to subscribe, and let me know what else you need. I’m always making more videos and I would love to make one just for you to answer your question.