Why do Seattle sellers reject VA loan offers? Most VA loan rejections in Seattle come down to seller misconceptions about appraisals, repair requirements, and closing timelines, not the buyer’s creditworthiness. In 2026, veteran buyers using the right strategy win competitive offers in King County and Pierce County regularly.

You served. You earned the VA loan benefit. And then a Seattle seller’s agent called to say they went with another offer.

This happens more than it should. And in most cases, the seller’s reluctance has nothing to do with you personally. It has to do with misunderstandings about how VA loans actually work, fears that have not been relevant for years, and agent-to-agent dynamics that a good buyer’s agent knows how to navigate.

This post covers the real reasons Seattle sellers pass on VA offers, what the 2026 numbers actually look like for King County and Pierce County veterans, and the specific strategies that get VA buyers into homes even in competitive bidding situations.

Why Seattle Sellers Pass on VA Loan Offers

Let us start with what sellers are actually thinking. Most of the hesitation falls into three buckets.

1. Appraisal Concerns

VA appraisals have a reputation for being stricter than conventional appraisals. There is some truth to this historically, but the gap has narrowed significantly. The bigger issue is seller perception. Many sellers and their agents assume a VA appraisal will come in low or flag conditions that kill the deal.

In practice, VA appraisers are looking for the same basic habitability standards that most lenders require. A home that would pass a conventional appraisal will almost always pass a VA one. The problems arise with properties that have genuine condition issues: exposed wiring, active roof leaks, broken HVAC, no working heat source.

2. The Escape Clause

The VA Escape Clause is a federal protection that allows a veteran buyer to walk away from a purchase if the property appraises below the purchase price. This clause cannot be waived. Sellers know this, and some see it as a risk that a conventional buyer does not carry.

What sellers often do not know is that a veteran buyer CAN choose to pay the difference between the appraised value and the purchase price out of pocket, the same way a conventional buyer would. The Escape Clause protects veterans. It does not prevent them from competing.

3. Closing Timeline Assumptions

VA loans have a reputation for closing slowly. This was more true ten years ago than it is today. With an experienced VA lender and a buyer who has their documents in order, a VA loan can close in 21-30 days, comparable to conventional financing. The reputation just has not caught up with the reality.

VA Loan Myths vs. Reality in Seattle

VA appraisals always kill the deal

VA appraisals flag the same issues most lenders would. Well-maintained homes pass routinely.

VA buyers cannot compete with cash or conventional offers

With the right agent, pre-approval, and offer structure, VA buyers win competitive situations regularly in King County.

The VA Escape Clause means the buyer can walk for any reason

The Escape Clause only applies if the appraisal comes in below the purchase price. It is a financial protection, not an open exit.

VA loans take forever to close

With a strong VA lender and organized buyer, 21-30 day closings are achievable in 2026.

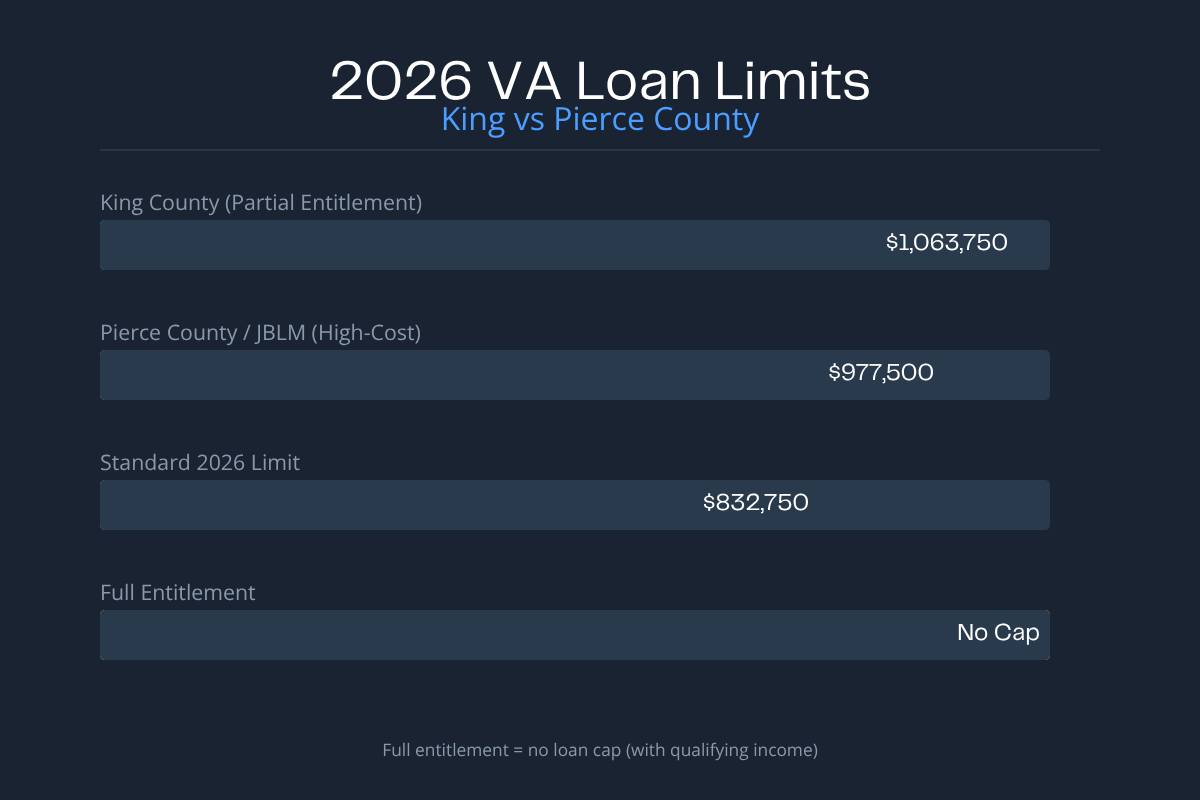

2026 VA Loan Limits in King County and Pierce County

Here is the data that matters for Greater Seattle and JBLM veterans in 2026.

The King County limit matters because the Seattle metro median sale price sits well above the national baseline. Veterans with full entitlement (no prior VA loan outstanding) have no loan limit at all and can purchase any price point with zero down, subject to lender approval and qualification. The limits above apply to veterans with partial entitlement.

How VA Buyers Win in the Seattle Market: A 6-Step Playbook

Here is what actually works when you are competing against conventional and cash buyers in Greater Seattle.

This is the single most important variable. A lender who closes VA loans in King County weekly knows the local appraisers, knows the timeline, and can give a seller’s agent the confidence that this deal will close. Ask your lender how many VA loans they closed in the Seattle market in the last 12 months. The answer tells you everything.

A fully underwritten pre-approval means the lender has reviewed your income, assets, credit, and military service documentation before you make an offer. This is as close to cash as a financed offer gets. It eliminates most of the risk a seller is worried about.

If the home is priced aggressively, consider including an appraisal gap addendum committing to pay a specific dollar amount above the appraised value. This directly addresses the seller’s biggest concern about the VA Escape Clause. It signals financial strength and seriousness.

Inspection contingencies, financing contingencies, and requests for seller concessions are all negotiating points where a VA offer can look weaker. Work with your agent to understand which contingencies are essential protections versus which are negotiable. A cleaner offer, even at a slightly lower price, often beats a messy higher one.

This is not always appropriate or legal in every context, but in competitive situations some sellers respond to knowing who is buying their home. Mentioning military service, the family you are building, or your connection to the area can shift a seller’s perspective. Your agent will know whether this is appropriate for a given listing.

A buyer’s agent who has successfully closed VA transactions in King County knows how to communicate your offer to a listing agent in a way that builds confidence. The agent-to-agent conversation that happens before the offer is reviewed matters more than most buyers realize. Positioning your offer as a well-prepared, low-risk transaction is a skill, not an accident.

Watch: Negotiation Strategies Every Seattle Buyer Needs to Know

I put this video together specifically for buyers navigating competitive situations in the Greater Seattle market. The negotiation principles apply directly to VA buyers going up against stronger-looking offers on paper.

VA Loan vs. Conventional: What Seattle Sellers Actually See

| Factor | VA Loan (2026) | Conventional (20% down) |

|---|---|---|

| Down payment | $0 with full entitlement | Typically 20% ($160K+ on $800K home) |

| Mortgage insurance | None | None at 20% down |

| Funding fee | 1.25%-3.3% (tax-deductible in 2026) | None |

| Appraisal requirements | VA appraisal required | Standard appraisal required |

| Escape Clause | Federal protection, cannot be waived | Appraisal contingency (can be waived) |

| Closing timeline | 21-30 days with experienced lender | 21-30 days typical |

| King County loan limit | $1,063,750 (partial entitlement) | $1,063,750 conforming |

A Note for JBLM Veterans and Pierce County Buyers

If you are stationed at Joint Base Lewis-McChord or relocating to the Pierce County area, the 2026 VA ceiling for your county is $977,500. That covers a significant portion of the market in Tacoma, Lakewood, and surrounding areas.

JBLM relocations have their own timeline pressures that Seattle area moves sometimes do not. If you are working with orders and a firm reporting date, your agent needs to understand how to compress the process without cutting corners on due diligence. This is a situation where experience with military relocations specifically matters, not just general buyer’s agent experience.

For a broader look at the current Greater Seattle market conditions affecting your buying timeline, see our monthly Seattle real estate market update.

If you are comparing neighborhoods for a relocation purchase, our guide on winning offer strategies for Seattle buyers covers the competitive dynamics across different submarkets.

You Earned This Benefit. Let’s Use It to Win.

Download the free guide: Using Your VA Entitlement for a plain-English breakdown of how the VA loan benefit works in Washington State.

Or text HOME to 206-245-8813 and I will send it directly to your phone.

Ready to talk strategy? Book a free buyer consultation: bit.ly/call-emily

Warmly, Emily

Emily Cressey | HomePro Associates at Keller Williams Greater Seattle | 206-245-8813 | homeproassociates.com

- $1,200,000

- 3 bd

- 3 ba

- 2000 sqft

Fully Remodeled Home with Sunset Views in Woodinville Wine Country

Pending

Pending

- $644,000

- 2 bd

- 1.5 ba

- 861 sqft

Shoreline Home with Detached Studio and Garden Space

Sold

Sold

- $1,350,000

- 3 bd

- 2.5 ba

- 2823 sqft

Private Northwest Retreat in Meadowdale Beach in Edmonds, WA

{kind=link}