Should you buy before you sell your Seattle home in 2026? For most Greater Seattle move-up buyers in 2026, selling first is the safer default. With mortgage rates in the low-6% range and more inventory than we have seen in years, carrying two homes is a real financial risk. That said, several tools including bridge loans, HELOCs, rent-backs, and buy-before-you-sell programs can make buying first work if your situation calls for it.

It is one of the most common questions move-up buyers ask: do I sell my current home first, or buy the next one first?

There is no universal answer. The right sequence depends on your financial cushion, your timeline, how much equity you have, and what the market is doing in your specific price range and neighborhood. What works in Kirkland may not work the same way in Bothell or South Snohomish County.

This guide walks through the real tradeoffs, the financing tools that give you more flexibility, and how Washington State’s home sale contingency process works, so you can make this decision with clear eyes.

The Core Problem: Two Transactions, One Timeline

Move-up buyers face a sequencing problem that first-time buyers and pure sellers do not. You need to sell one asset and buy another, ideally without a gap in housing or a period of carrying two mortgages.

Both outcomes — selling too early and being temporarily homeless, or buying too early and being stretched thin — can be stressful and expensive. Most of the strategy in this guide is about reducing the risk of both.

Sell First vs. Buy First: The Real Tradeoffs

| Factor | Sell First | Buy First |

|---|---|---|

| Financial risk | Lower: you know exactly what you net before committing | Higher: carrying two mortgages if your home does not sell quickly |

| Negotiating strength | Strong: non-contingent offer on your next home | Weaker: sellers may reject or discount contingent offers |

| Housing gap risk | Real: you may need temporary housing between transactions | Low: you move directly from one home to the next |

| Down payment clarity | Clear: you know your equity before you shop | Uncertain: equity is locked until your home closes |

| Best market for this approach | Any market, especially when rates are elevated | Fast-moving seller’s market where contingent offers rarely win |

| 2026 Seattle recommendation | Default choice for most buyers | Viable with the right financing tools in place |

Emily’s Take

In 2026, I recommend sell-first as the default for most of my move-up clients. Inventory is up, which means your next home is more likely to be available when you are ready. Carrying two mortgages in a higher-rate environment is a real stress test on a household budget. That said, if you have strong cash reserves or access to bridge financing, buying first is absolutely doable. Let’s look at your numbers specifically before deciding.

4 Ways to Bridge the Gap If You Want to Buy First

If selling first is not practical for your situation, these are the tools that give move-up buyers flexibility.

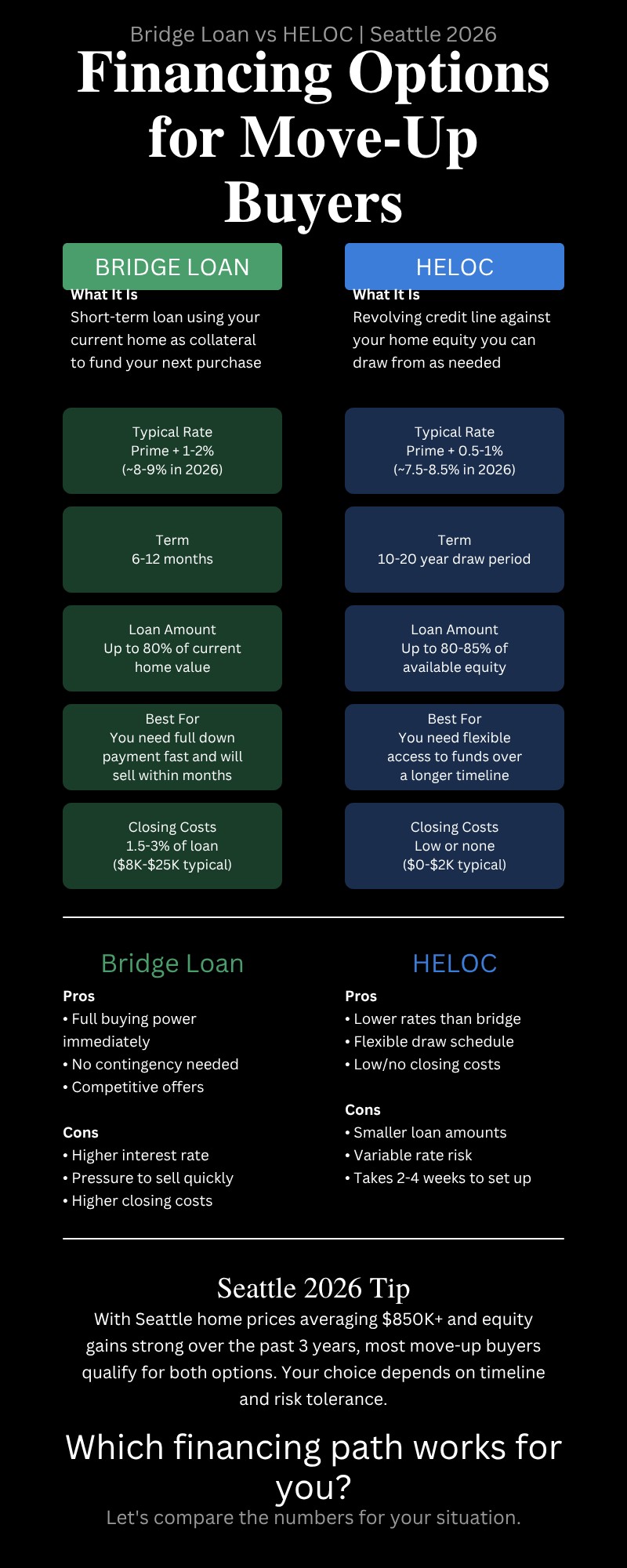

A short-term loan secured by your current home that gives you cash to close on your next purchase before your current home sells. Bridge loans typically run 6-12 months and carry higher rates than standard mortgages. They work well when your home has substantial equity and you are confident it will sell quickly. Not all lenders offer them, and qualification can be strict. Ask your lender specifically whether they originate bridge loans in Washington State.

A line of credit against your current home’s equity that you draw on for the down payment on your next purchase. HELOCs are generally less expensive than bridge loans and more flexible. The catch: you need to get the HELOC in place before you list your current home, because most lenders will not approve a new HELOC on a home that is actively listed for sale. Plan ahead by at least 60-90 days if this is your strategy.

Refinancing your current mortgage for more than you owe and taking the difference as cash for your next down payment. In a higher-rate environment like 2026, this only makes sense if your current mortgage rate is already at or above current rates, or if the equity access is worth the cost. Run the numbers carefully with your lender before going this route.

Several companies offer programs that purchase your next home on your behalf or provide a guaranteed offer on your current home, giving you non-contingent buying power without needing to sell first. These programs have improved significantly and are worth exploring if you have a specific home you do not want to lose. Fees and terms vary, so compare carefully. Your agent can walk you through the options available in the Greater Seattle market.

Using a Rent-Back to Buy Time

A rent-back agreement lets you sell your current home and then rent it back from the buyer for a set period, typically 30-60 days, while you complete the purchase of your next home. This eliminates the housing gap entirely.

Rent-backs are negotiated as part of the sale contract. You pay the buyer a daily rent amount (usually based on their mortgage payment) for the agreed period. The buyer gets the sale closed; you get time to move without pressure.

Not every buyer will agree to a rent-back, especially if they have their own move-in deadline. But in a market with more inventory and less buyer urgency, sellers have more room to ask. Your agent should know how to present a rent-back request in a way that does not kill an otherwise good offer.

Washington Form 22B: The Home Sale Contingency

If you choose to make an offer on a new home before your current one is sold, Washington State’s NWMLS Form 22B is the standard home sale contingency addendum. It makes your purchase contingent on the sale and closing of your current home within a specified timeframe.

Sellers can accept, reject, or counter a contingent offer. In competitive situations, contingent offers often lose to non-contingent ones at the same price. But with more inventory in 2026, more sellers are willing to consider them, especially if the buyer’s home is already listed and in good shape.

For a deeper look at how contingencies work in Washington State transactions, see our guide: Contingencies When Buying or Selling a House in the Seattle Area.

The Form 22B also includes a “bump clause” provision, which allows the seller to keep marketing the home and potentially bump your contingent offer if a better non-contingent offer comes in within a set notice period, typically 3-5 days. Understanding this clause before you sign is important.

Know Your Numbers Before You Decide

The buy-vs-sell-first decision ultimately comes down to your financial position. Before committing to either path, get clear on three numbers:

- Your net proceeds from the current home: What will you actually walk away with after mortgage payoff, closing costs, and commissions? See our breakdown of closing costs in Seattle and download The Real Cost of Selling Your Home for the full picture.

- Your target purchase price and down payment requirement: What do you need to put down on your next home, and can you get there without the sale proceeds in hand?

- Your carrying cost tolerance: If your current home takes 45-60 days to sell after you have already bought, can your budget absorb two mortgage payments for that period without serious strain?

For a comprehensive look at the current buying environment in King and Snohomish County, see our Seattle home buying analysis.

And if you missed our Move-Up Buyer Class, the key takeaways are available here: Move-Up Buyer Class recap.

Watch: Your Step-by-Step Seattle Home Buying Plan

This video walks through the full buying process in Greater Seattle, including the sequencing decisions move-up buyers face. If you are coordinating a sale and a purchase at the same time, the timeline section is especially relevant.

Let’s Map Out Your Move-Up Plan.

The buy-vs-sell-first decision looks different for every household. Download The Real Cost of Selling Your Home to get clear on your net proceeds before you start shopping.

Or book a free move-up buyer consultation: bit.ly/call-emily

Questions? Call or text: 206-245-8813

Warmly, Emily

Emily Cressey | HomePro Associates at Keller Williams Greater Seattle | 206-245-8813 | homeproassociates.com

Tell Us What You Need!

We would love to hear from you! Please fill out this form and we will get in touch with you shortly.