Buying a home is one of the most exciting things you’ll do in your life. It’s also likely the most expensive. Unless you have a swimming pool full of cash, you’ll need to take out a mortgage to help finance the purchase of a home.

Applying for a mortgage can be nerve-wracking, especially if you’re doing it for the first time. Applying for a home loan is never simple and always causes a lot of anxiety. No one wants to spend months searching for that dream home only to find out late in the process that they can’t get sufficient or any financing. The best thing you can do, then, is to do everything possible to stack the odds in your favor early on. So check out these 5 things you can do right now to secure a home loan in Shoreline, WA.

1. Determine What You Can Afford

Before you get your sights set on your dream home, make sure you can afford it.

Your first step toward securing a home loan in Shoreline, WA should be determining exactly what you can afford. Your lender certainly will, so it pays to do this early on in the process.

A good way to proceed here is by “using the 28/36 rule. This refers to your debt-to-income ratio or the total amount of your gross monthly income that’s allocated to paying debt each month. For example, a 50% DTI means you spend half of your monthly pre-tax income on debt repayment. Ideally, your front-end’ DTI, which includes only your mortgage-related expenses, should be below 28%. Your ‘back-end’ ratio, which includes the mortgage and all other debt obligations, should be no more than 43%, though under 36% is ideal.”

If, after doing these calculations, your DTI turns out to be too high, you’ll need to work on getting it down or maybe even look at a more affordable home. Contact a Shoreline, WA agent at (206) 245 8813 for expert assistance in determining affordability and thus improving your chances of securing a home loan in Shoreline, WA.

And remember, too, that your monthly mortgage payment isn’t the only thing to consider. You’ll also need to factor in interest, insurance, property taxes, HOA fees, utilities, maintenance and repairs, and private mortgage insurance.

2. Work on Your Credit Score

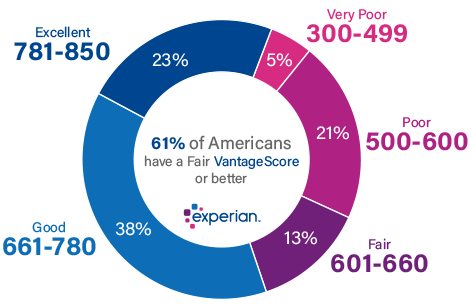

Your credit reports don’t contain your credit scores. Fortunately, it’s fairly easy to get your credit score for free. Maybe the most important thing you can do right now to secure a home loan in Shoreline, WA is to improve your credit score.

For most conventional loans, you’ll need a minimum score of 620 to 640. With some government-backed loans, you may be able to get by with a score as low as 500 – if you meet certain other qualifying criteria. No matter the kind of loan, though, it will be more affordable with a higher score.

Here’s what industry experts say about improving your credit score to get a home loan in Shoreline, WA: “One of the best ways to improve your credit score is to make all your debt payments on time and in full. Payment history – the most heavily weighted factor – accounts for 35% of your credit score. The amount of debt you owe in relation to the total amount of credit extended to you contributes to another 30% of your score, so it’s best to keep your debt as low as possible.”

And you certainly want to avoid doing anything that can damage your credit score. So don’t make any major purchases that require credit, and don’t open any new lines of credit.

3. Save Some Cash

You also need to have some cash saved up if you want to secure a home loan in Shoreline, WA. And you can, of course, begin working on that right now.

Lenders are cautious and always look out for their interests first. If you don’t have a good amount of cash reserves, you may not get a home loan. The main reason for this is that you have to be able to make a down payment and cover the closing costs, inspection, appraisal, and so on.

Here’s what you can expect with respect to the down payment: “[Minimums vary and depend on various factors, such as the type of loan and the lender. Each lender establishes its own criteria for down payments, but on average, you’ll need at least a 3.5% down payment. Aim for a higher down payment if you have the means. A 20% down payment not only knocks down your mortgage balance, but it also alleviates private mortgage insurance or PMI.”

4. Pay Off Debt and Avoid New Debt

Another credit-score-related thing you can do to secure a home loan in Shoreline, WA is to pay down your existing debt and avoid taking on new debt. You don’t have to have a zero credit card balance, but the less you owe, the better off you’ll be.

We’ve already talked about the debt-to-income ratio and how you need to get that down below a certain threshold. Paying off debt is one way to do that. But you also have to avoid those tempting major purchases like new furniture and/or appliances for your new home. Here’s why…

“Even if you’re approved for a mortgage with consumer debt, it’s important to avoid new debt while going through the mortgage process. Lenders recheck your credit before closing, and if your credit report reveals additional or new debts, this can stop the mortgage closing. As a rule, avoid any major purchases until after you’ve closed on the mortgage loan.”

5. Keep Your Job

Also, to ensure you get a home loan in Shoreline, WA, you need to keep your job. Now, this doesn’t just mean you shouldn’t stop working, You shouldn’t change jobs either – even for a higher-paying job.

“Sticking with your employer while going through the home buying process is crucial. Any changes to your employment or income status can stop or greatly delay the mortgage process.”

After You Get a Home Loan in Shoreline, WA

Securing a mortgage is one of many steps in the overall home buying process, but it’s an important one. Be sure to take the time to evaluate your options carefully. After all, 30 years is a long time to spend locked into an expensive loan.

Once you have the loan approval, you’re on the home stretch. All that’s left is to prepare for closing day. That means doing a final walk-through of your home, securing homeowners and title insurance, getting a cashier’s check for your down payment, and warming up your contract-signing arm.

Do these things, and you’ll likely get your home loan. But what comes after that – after you know you can get the financing you need? You don’t want to squander that hard-won loan on a home that doesn’t suit you or winds up costing you a ton of money. That’s when you need to call on the expertise of your local real estate agent. So if you’ve secured a home loan in Shoreline, WA and are ready to take the next step, contact us today at (206) 245 8813.

{kind=link}